If you’ve ever dreamed of owning an investment property, you’re not alone! Many people are eager to dive into the world of real estate and make their money work for them. But the big question is: how do you finance an investment property? Don’t worry, I’ve got you covered. In this article, we’ll explore the ins and outs of financing an investment property and provide you with some expert tips to get you started on your real estate journey.

When it comes to financing an investment property, there are several options available to you. From traditional mortgages to creative financing strategies, the possibilities are endless. But before we dive into the nitty-gritty details, let’s first understand what an investment property is. Simply put, it’s a property that you purchase with the sole intention of generating income. This could include rental properties, vacation homes, or even commercial real estate. Now that we’ve got that cleared up, let’s explore the different ways you can finance your investment property and turn your real estate dreams into a reality. So grab a cup of coffee, sit back, and let’s get started!

How to Finance an Investment Property

Step 1: Assess your financial situation and determine how much you can afford to invest in a property.

Step 2: Research financing options such as traditional mortgages, private lenders, or government-backed loans.

Step 3: Gather all necessary documentation, including proof of income, credit history, and property details.

Step 4: Apply for pre-approval from lenders to determine your borrowing capacity.

Step 5: Compare interest rates, terms, and conditions from different lenders to find the best financing option.

Step 6: Submit your loan application and provide any additional information or documentation required.

Step 7: Once approved, review the loan agreement carefully and ensure you understand all terms and conditions.

Step 8: Close the deal by signing the loan agreement and completing any additional requirements.

How to Finance an Investment Property: A Comprehensive Guide

Investing in real estate can be a lucrative venture, but it often requires a significant upfront investment. If you’re looking to finance an investment property, you’re in the right place. In this guide, we’ll explore various financing options and strategies to help you make the most of your investment. From traditional mortgages to alternative funding sources, we’ll cover everything you need to know to secure financing for your investment property.

Understanding Traditional Mortgage Options

When it comes to financing an investment property, traditional mortgages are a popular choice. These mortgages are similar to those used for primary residences, but there are a few key differences to keep in mind.

Firstly, lenders often require a larger down payment for investment properties compared to primary residences. While you may be able to secure a mortgage with as little as 3% down for a primary residence, investment properties typically require a down payment of 20% or more. This larger down payment helps mitigate the higher risk associated with investment properties.

Additionally, interest rates for investment property mortgages may be slightly higher than those for primary residences. Lenders consider investment properties to be riskier investments, so they may charge a slightly higher interest rate to compensate for this risk. However, keep in mind that interest rates can vary depending on your financial profile and the current market conditions.

Exploring Alternative Financing Options

While traditional mortgages are a popular choice, they’re not the only option for financing an investment property. Alternative financing options can provide additional flexibility and opportunities for investors. Let’s take a closer look at some of these alternatives:

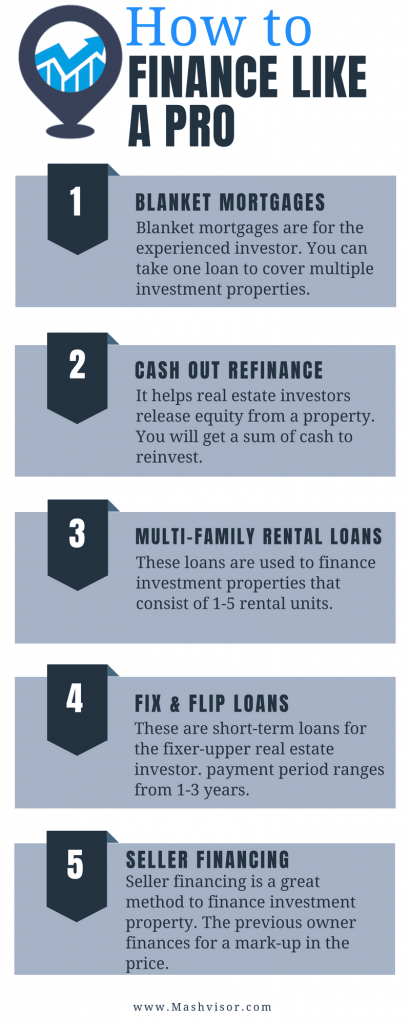

1. Hard Money Loans: Hard money loans are short-term, high-interest loans that are often used by real estate investors. These loans are typically provided by private investors or companies and are secured by the property itself. Hard money loans can be a viable option for investors who need quick financing or have less-than-ideal credit scores.

2. Seller Financing: In some cases, sellers may be willing to finance the purchase of their property directly. This means that instead of obtaining a traditional mortgage from a bank, the buyer makes payments directly to the seller. Seller financing can be a win-win situation, offering flexibility for the buyer and potential income for the seller.

3. Home Equity Loans or Lines of Credit: If you already own a primary residence with significant equity, you may be able to tap into that equity to finance your investment property. Home equity loans or lines of credit allow you to borrow against the value of your home, providing funds for your investment property purchase.

It’s important to carefully consider the terms and conditions of any alternative financing options. While they can offer flexibility, they may also come with higher interest rates or shorter repayment terms. Be sure to weigh the pros and cons before making a decision.

The Benefits of Financing an Investment Property

Now that we’ve explored different financing options, let’s discuss the benefits of financing an investment property.

1. Leverage: Financing allows you to leverage your investment by using borrowed money to acquire the property. This can significantly increase your potential returns, as you’re not solely reliant on your own funds.

2. Property Appreciation: Real estate has the potential to appreciate over time, meaning the value of your investment property could increase. By financing the property, you can benefit from this appreciation without tying up all of your own capital.

3. Diversification: Investing in real estate provides diversification within your investment portfolio. By adding an income-generating property to your portfolio, you can reduce risk and potentially increase your overall returns.

Financing vs. Paying Cash: Which Is Right for You?

When it comes to financing an investment property, one of the key decisions you’ll need to make is whether to finance the purchase or pay cash. Both options have their advantages and considerations.

Financing: Financing allows you to conserve your own capital and potentially invest in multiple properties. It also provides the opportunity to take advantage of leverage and potentially increase your returns. However, it comes with the added cost of interest payments and the need to qualify for a mortgage.

Paying Cash: Paying cash for an investment property offers the benefit of no interest payments and greater flexibility. You won’t have to worry about mortgage approvals or making monthly payments. However, this approach requires a significant upfront investment and may limit your ability to invest in multiple properties.

Ultimately, the decision between financing and paying cash depends on your financial situation, investment goals, and risk tolerance. Consider consulting with a financial advisor or real estate professional to help you make the best decision for your specific circumstances.

Tips for Financing an Investment Property

Now that we’ve covered the basics of financing an investment property, let’s explore some tips to help you navigate the process successfully.

1. Improve Your Credit Score: A higher credit score can help you secure more favorable interest rates and terms for your investment property loan. Take steps to improve your credit score, such as paying off debts and monitoring your credit report.

2. Save for a Larger Down Payment: As mentioned earlier, investment properties typically require a larger down payment. Saving for a larger down payment can help you secure better financing terms and reduce the overall cost of your investment.

3. Research Lenders: Not all lenders offer investment property financing, so it’s important to research and find lenders who specialize in this type of loan. Compare interest rates, fees, and loan terms to ensure you’re getting the best deal possible.

4. Consider Partnership Opportunities: If you’re short on funds or want to spread the risk, consider partnering with other investors. Pooling resources can make it easier to secure financing and diversify your investment portfolio.

5. Have a Solid Business Plan: Lenders will want to see a detailed business plan for your investment property. Include information on rental income projections, expenses, and your overall investment strategy.

By following these tips, you’ll be better prepared to finance your investment property and maximize your potential returns.

Conclusion

Financing an investment property opens up a world of opportunities for real estate investors. Whether you choose a traditional mortgage or explore alternative financing options, it’s important to carefully consider your options and make informed decisions. By understanding the benefits, weighing the pros and cons, and following some key tips, you’ll be well on your way to successfully financing your investment property. Happy investing!

Key Takeaways: How to Finance an Investment Property?

- 1. Start by saving for a down payment, aiming for at least 20% of the property’s purchase price.

- 2. Research different loan options, such as conventional mortgages or FHA loans, to find the best fit for your financial situation.

- 3. Improve your credit score by paying bills on time, reducing debt, and addressing any errors on your credit report.

- 4. Consider working with a mortgage broker who can help you navigate the lending process and find competitive interest rates.

- 5. Be prepared to provide detailed documentation of your income, assets, and financial history when applying for a loan.

Frequently Asked Questions

1. What are the different financing options available for investment properties?

When it comes to financing an investment property, there are several options available. Here are a few popular ones:

1. Conventional Loans: These are traditional mortgage loans offered by banks and lending institutions. They typically require a down payment of around 20% and have fixed interest rates.

2. Hard Money Loans: These are short-term loans provided by private lenders or investors. They are based on the value of the property rather than the borrower’s creditworthiness. However, they often come with higher interest rates and fees.

2. How can I improve my chances of getting approved for a loan for an investment property?

Getting approved for a loan for an investment property can be challenging, but there are steps you can take to improve your chances:

1. Improve your credit score: A higher credit score demonstrates your creditworthiness and makes you a more attractive borrower.

2. Save for a larger down payment: A larger down payment shows the lender that you have a vested interest in the property and reduces the risk for them.

3. What is the difference between a fixed-rate mortgage and an adjustable-rate mortgage?

A fixed-rate mortgage has an interest rate that remains the same throughout the life of the loan. This provides stability and predictable monthly payments. On the other hand, an adjustable-rate mortgage (ARM) has an interest rate that can change periodically. It may start with a lower rate initially but can increase over time.

Choosing between the two depends on your financial situation and risk tolerance. If you prefer stability and predictability, a fixed-rate mortgage may be the better option. If you expect interest rates to decrease or plan to sell the property before the rate adjusts, an ARM may be more suitable.

4. Can I use a home equity loan to finance an investment property?

Yes, you can use a home equity loan to finance an investment property. A home equity loan allows you to borrow against the equity you have built in your primary residence. However, keep in mind that if you default on the loan, you risk losing your primary residence. It’s important to carefully consider the risks and benefits before using a home equity loan for investment property financing.

5. What is private financing for investment properties?

Private financing for investment properties involves obtaining a loan from an individual or a private lending institution. This type of financing may be more flexible and have fewer stringent requirements compared to traditional loans. However, it often comes with higher interest rates and fees. Private financing can be a viable option for investors who may not qualify for conventional loans or need quick access to funds.

Final Summary: Financing an Investment Property Made Easy

So, you’ve learned all about how to finance an investment property, and now you’re ready to take the plunge into the world of real estate investing. Congratulations! In this final summary, let’s quickly recap the key points and highlight the importance of proper financing for your investment endeavors.

First and foremost, it’s crucial to have a solid understanding of your financial situation and goals. Whether you choose traditional financing options like mortgages or explore alternative methods such as hard money loans or private lenders, knowing your budget and risk tolerance is essential. Remember, investing in real estate is a long-term game, so it’s vital to choose a financing option that aligns with your investment strategy and supports your overall financial objectives.

Next, don’t forget to consider the potential return on investment (ROI) and cash flow of the property. Conduct thorough research and analysis to determine if the property has the potential to generate positive cash flow and appreciate in value over time. This will not only help you secure financing but also ensure that you’re making a sound investment decision.

Lastly, stay up-to-date with the latest financing options and market trends. Real estate financing is constantly evolving, and new opportunities may arise that could benefit your investment strategy. Keep a close eye on interest rates, loan terms, and any government initiatives that may provide incentives for real estate investors.

In conclusion, financing an investment property doesn’t have to be daunting. With careful planning, a clear understanding of your goals, and an awareness of the available financing options, you can navigate the world of real estate investing with confidence. Remember to always do your due diligence, seek professional advice when needed, and make informed decisions based on your unique circumstances. Now, it’s time to put your newfound knowledge into action and start building your real estate portfolio. Happy investing!